What are the biggest expenses you’ll face in retirement? Healthcare? Housing? Travel? All of those costs could be significant, but one of the biggest could be taxes. That’s right. Just because you’re done working, doesn’t mean you’re done paying taxes.

Many sources of retirement income, like Social Security, pensions, and retirement account distributions, are taxable. That doesn’t even include the wide range of other taxes you could face, like property taxes, sales tax, and more. Taxes may be a part of life, but they can also be a drain on your retirement. Every dollar you pay in taxes is a dollar that can’t be used to support your lifestyle and fund your goals. Fortunately, you can take action to reduce your tax burden and maximize your retirement income. Below are five steps to consider as you approach retirement: 1) Use a Roth IRA. A traditional IRA is an effective savings vehicle for retirement. You get tax-deferred growth, and potentially tax deductions for your contributions. However, a traditional IRA can also create tax issues in retirement. Most distributions from a traditional IRA are taxed as income. If you use an IRA to accumulate a sizable nest egg, you could face taxes on much of your income in retirement. The alternative is a Roth IRA. In a Roth IRA, you don’t get tax deductions when you make a contribution. However, your distributions in retirement are tax-free, assuming you are at least age 59 ½ and you have held the Roth for at least five years. As a married couple, you cannot contribute to a Roth if your income is greater than $196,000 in 2020. For a single person, that limit is $124,000.1 Otherwise, you can contribute up to $6,000 this year, or up to $7,000 if you’re 50 or older.2 You can also convert your traditional IRA to a Roth. This means paying taxes on the traditional IRA amount. However, after the conversion, you can grow the remaining assets in the Roth on a tax-free basis and take tax-free distributions in retirement. 2) Be strategic about Social Security distributions. Social Security will likely play a role in your retirement income puzzle. However, taxes will impact the net amount you receive from Social Security. The extent that your Social Security benefit is taxed depends on a number called your “combined income.” Combined income is your adjusted gross income plus nontaxable interest plus half of your Social Security benefit.3 If you are single and your combined income is between $25,000 and $34,000, up to 50% of your benefits could be taxable. If you earn more than $34,000, up to 85% of your benefits could be taxable.3 For married couples, if your combined income is between $32,000 and $44,000, up to 50% of your benefits could be taxed. If you earn more than $44,000, up to 85% of your benefits could be taxed. The key to reducing your combined income is to reduce your adjusted gross income. Non-taxable income is not included in that number. So, for example, you could maximize your Roth IRA to minimize your adjusted gross income. You could also delay Social Security until age 70 to increase your benefit, and draw down your taxable accounts, like a traditional IRA, before Social Security starts. 3) Consider downsizing. Simply moving to a new home could reduce your taxes. Property taxes may be a major tax burden depending on your home. If you no longer need a large home, consider moving to something smaller that has a lower value and thus lower property taxes. You also may look at a neighboring community that has a lower property tax rate. 4) Relocate to a more tax-friendly state. Another option is to move to another state completely. Some states are more tax-friendly for retirees than others. For example, Alabama doesn’t tax Social Security benefits and has a relatively low sales tax rate.4 Florida is another option as it doesn’t have a state income tax.5 Do your research and you may find a new home that is appealing and saves you money. 5) Use an HSA to pay for medical costs. Fidelity estimates that the average 65-year-old couple will pay $285,000 out-of-pocket for health care expenses in retirement.6 If you’re using taxable distributions from an IRA or 401(k) to pay those costs, the impact on your savings could be even greater. One strategy to minimize the tax burden is to use a health savings account (HSA) to pay for healthcare costs. In 2020, individuals can contribute up to $3,550 to an HSA. Families can contribute up to $7,100.7 You can invest and allocate those funds to match your goals and risk tolerance. The assets grow on a tax-deferred basis as long as they stay in the account. When you’re ready to use the funds, you can take tax-free distributions to pay for qualified healthcare expenses like premiums, deductibles, copays, and more. By using a tax-free source to pay for healthcare costs, you reduce the amount you need to take from taxable accounts, like an IRA or 401(k). That, in turn, reduces your overall tax burden. A financial professional can help you determine if an HSA is right for you. Ready to develop your retirement tax strategy? Let’s talk about it. Contact us today at Walker · Wells. We can help you analyze your needs and develop a plan. 1https://www.irs.gov/retirement-plans/plan-participant-employee/amount-of-roth-ira-contributions-that-you-can-make-for-2020 2https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits 3https://www.ssa.gov/benefits/retirement/planner/taxes.html#:~:text=Learn%20Apply%20Manage-,Income%20Taxes%20And%20Your%20Social%20Security%20Benefit,on%20your%20Social%20Security%20benefits.&text=between%20%2425%2C000%20and%20%2434%2C000%2C%20you,your%20benefits%20may%20be%20taxable. 4https://money.usnews.com/money/retirement/baby-boomers/slideshows/the-most-tax-friendly-states-to-retire?slide=2 5https://money.usnews.com/money/retirement/baby-boomers/slideshows/the-most-tax-friendly-states-to-retire?slide=4 6https://www.cnbc.com/2019/04/02/health-care-costs-for-retirees-climb-to-285000.html 7https://www.shrm.org/resourcesandtools/hr-topics/benefits/pages/irs-2020-hsa-contribution-limits.aspx The information contained herein is based on our understanding of current tax law. The tax and legislative information may be subject to change and different interpretations. We recommend that you seek professional legal advice for applicability to your personal situation. Licensed Insurance Professional. This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation. By providing your information, you give consent to be contacted about the possible sale of an insurance or annuity product. This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. This information has been provided by a Licensed Insurance Professional and is not sponsored or endorsed by the Social Security Administration or any government agency. 20277 - 2020/7/20  On March 27, President Trump signed the Coronavirus Aid, Relief, and Economic Security Act, which provides economic support to Americans who have been impacted by the coronavirus pandemic. You’re probably familiar with the highlights of the bill:

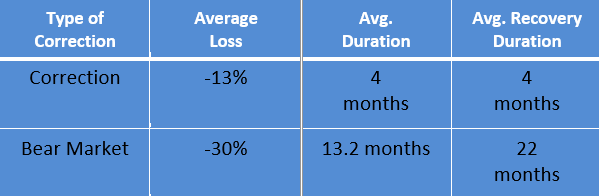

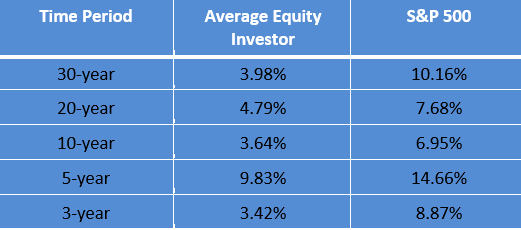

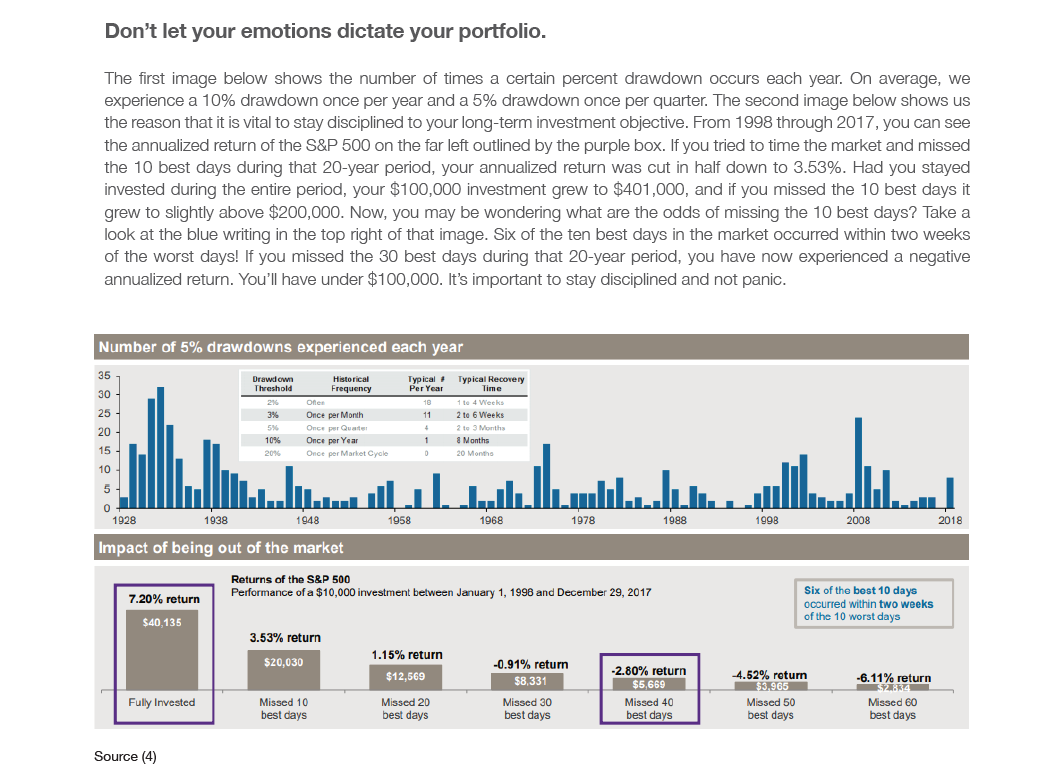

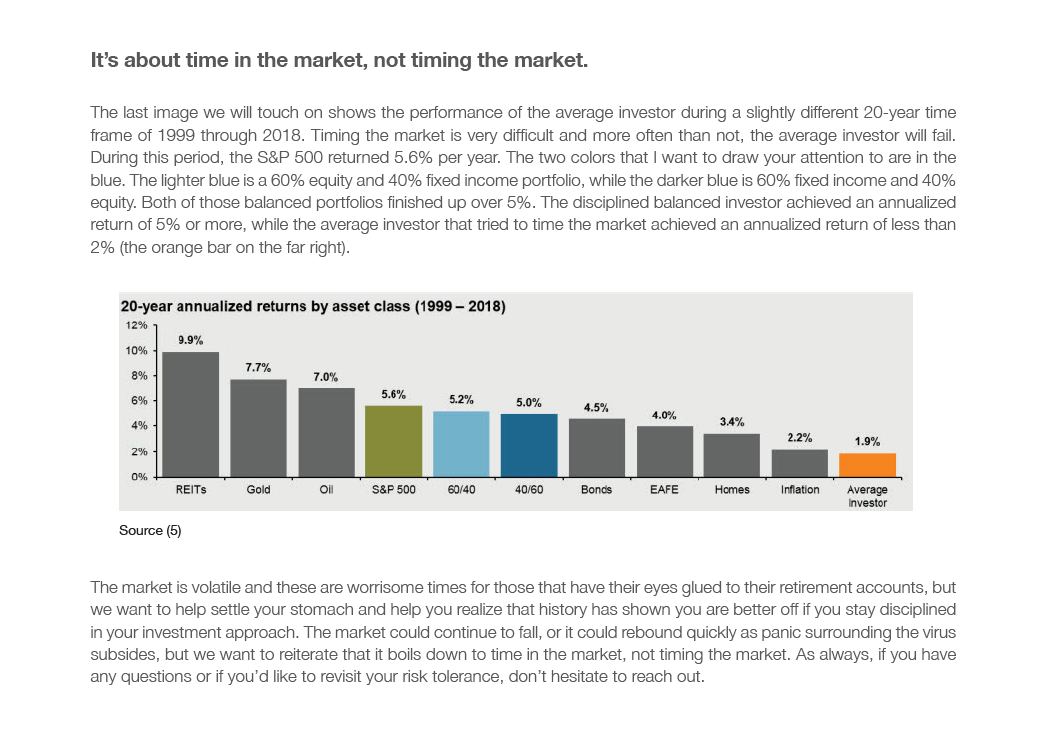

Those components are important and will certainly help many people get through this unprecedented period. However, there are some other provisions that could be important for you, especially if you’re approaching retirement or are already retired. Extended Tax Filing and IRA Deadline The IRS pushed back the tax filing deadline to July 15 from the traditional April 15.2 That gives you more time to prepare your return, collect documents, and possibly implement a strategy to minimize your tax bill. That also gives you more time to contribute to your IRA. You can make an IRA contribution up to July 15 and count it as a deduction on your 2019 return, assuming of course that you meet income requirements.3 401(k) and IRA Distribution Options It’s possible that you may need additional funds to get you through this period, especially if you or your spouse have been furloughed or have lost income. The CARES Act allows you to tap into your qualified retirement accounts through special distributions. You can take a withdrawal from your 401(k) and IRA without paying the 10% early distribution penalty, even if you are under age 59 ½. The distributions are taxable, but the taxes are spread over a three-year period. However, you can also repay the distribution over that three-year period and avoid paying taxes on the distribution.3 While a 401(k) or IRA distribution may be helpful, it could also have long-term consequences. When you take a distribution from your account, those funds are no longer invested. That means those funds can’t compound and grow. It’s possible that you may not fully participate in a market recovery if you decide to take a distribution, which could hurt your long-term growth. Waiver of RMDs Are you required to take an RMD in 2020? Not anymore. The CARES Act waives all RMDs in 2020, so there is no penalty for not taking a minimum distribution from a 401(k) or IRA. 4 This could be very helpful for your account balance. Your RMD would have been based on your December 31, 2019. Depending on how you are allocated, your account value may have been significantly higher on that date than it is today. That means that had the RMD not been waived, you would have potentially been required to take a substantial withdrawal from an account that had fallen in value.4 This may be a confusing and unprecedented time, but you have options available. We are here to help you explore those options and implement the right strategy for your retirement needs and goals. Contact us today at Walker · Wells. Let’s connect and start the conversation. 1https://www.thebalance.com/2020-stimulus-coronavirus-relief-law-cares-act-4801184 2https://www.irs.gov/coronavirus 3https://www.marketwatch.com/story/this-is-how-the-2-trillion-coronavirus-stimulus-affects-retirees-and-those-who-one-day-hope-to-retire-2020-03-31 4https://www.aarp.org/money/investing/info-2020/cares-act-retiree-tax-benefit.html Licensed Insurance Professional. This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation. By providing your information, you give consent to be contacted about the possible sale of an insurance or annuity product. This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. This information has been provided by a Licensed Insurance Professional and is not sponsored or endorsed by the Social Security Administration or any government agency. 19977 - 2020/4/7  The 2020 election cycle is in full swing. It’s primary season, which means the general election is right around the corner. Before you know it, the two major parties will have their conventions and we’ll be heading to the ballot box. Of course, you may already have election fatigue. From the local level all the way up to national races, candidates are already flooding television with political ads. As is the case in most presidential elections, candidates are also talking about the economy. They may make claims about what will happen in the economy if they’re elected or that the markets might decline if their opponent is elected. That kind of rhetoric is common during elections, but is it accurate? Will the outcome of the election impact your portfolio? Should you worry about the election? Or perhaps even change your allocation to protect yourself. Below are a few tips to keep in mind through the rest of the election year: Keep history in perspective. Often when there is one issue or story dominating the news, like the presidential election, it’s easy to focus solely on that story. It’s in the news and on social media so much that it feels like it’s the most important issue in the world. However, the truth is that this country and the stock market have been through many presidential elections. In fact, in most of those years, the markets performed positively. In fact, since 1928, there have been 23 presidential elections. In 19 of those years, the S&P 500 had a positive return.1 In fact, in the four instances when the markets did have negative returns, there were also economic events happening that may have driven the performance. In 1932, the country was in the midst of the Great Depression. In 1940, the country was entering World War II. The markets declined in 2000, which was the year George W. Bush ran against Al Gore. However, the bursting tech bubble in Silicon Valley may have had more influence on the markets than the election. Finally, in 2008, the S&P 500 also declined, but that was the year of the financial crisis. The takeaway is that market declines can happen in any year. The fact that it’s an election year may cause news stories and rhetoric, but the market is likely driven by investor concerns and economic conditions. Focus on the long-term. Your investment strategy was likely designed for the long-term. Perhaps you’re saving for retirement or some other goal that is years or possibly even decades in the future. Over that period, you’ll likely see times of market volatility. Whether it’s an election year or not, it’s always helpful to focus on the long-term during challenging periods. Market downturns happen, but they are always temporary. There are two common types of downturns: corrections and bear markets. Corrections are losses of 10% or more. Bear markets are losses of 20% or more. As you can see in the chart below, the average correction loses around 13% and the average bear market sees a loss of around 30%.2 However, the duration of each is also important. A correction, on average, lasts around four months. After that period, there is an average four-month recovery period to recoup the losses. Bear markets last longer. They have an average duration of 13 months with a 22-month recovery period.2  Market downturns are never pleasant, but they are temporary. Keep an eye on the long-term and stick to your strategy. Don’t make gut decisions. It can be easy to make a gut, impulse decision when you hear and see stressful news on a regular basis. It might be tempting to sell your investments and move to asset classes that have less risk and volatility. However, a move to perceived safety could do more harm than good. The chart below shows how the average equity investor has fared compared the S&P 500 over different periods of time. As you can see, the index always wins, sometimes by a wide margin. 3  Why does this happen? Primarily because the index stays invested at all times, while the average investor is constantly moving in and out of the market based on gut decisions or attempts to avoid loss. While investors may miss some declines with this strategy, they also miss out on gains. Staying invested usually leads to better long-term performance.

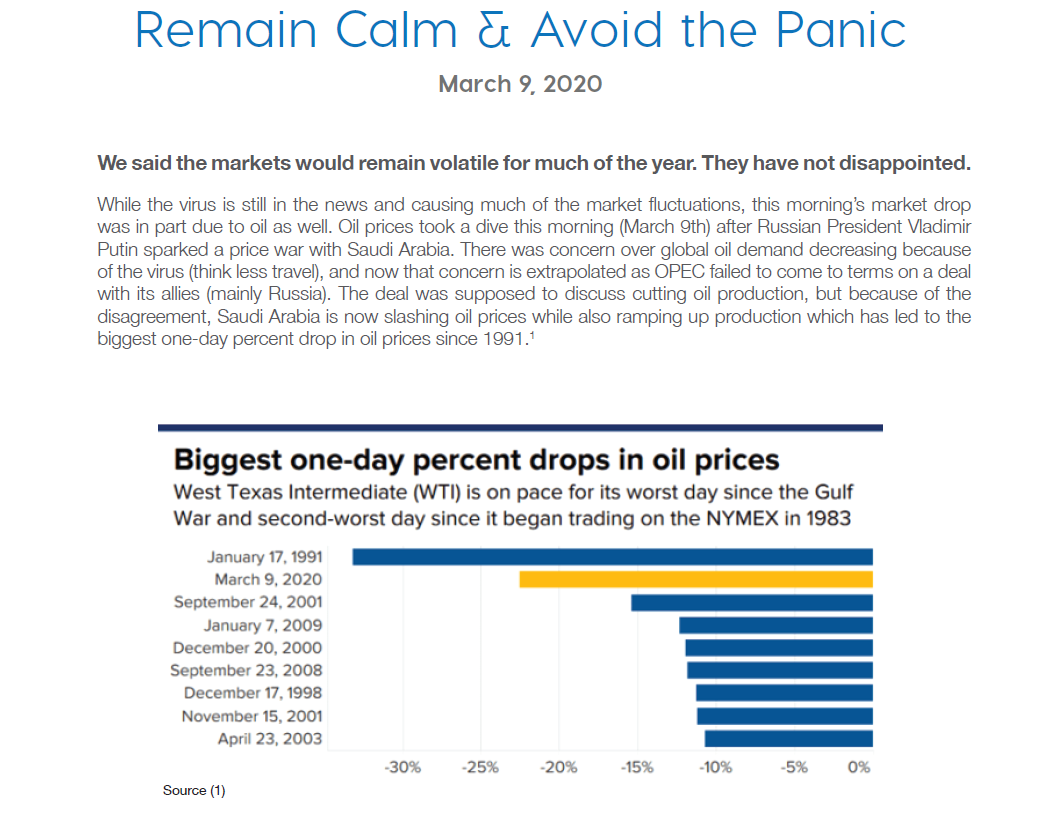

Ready to protect your portfolio this election year? Let’s talk about it. Contact us at Walker · Wells. We can help you analyze your needs and develop a strategy. Let’s connect soon and start the conversation. 1https://www.thebalance.com/presidential-elections-and-stock-market-returns-2388526 2https://www.cnbc.com/2018/12/24/whats-a-bear-market-and-how-long-do-they-usually-last-.html] 3https://www.marketwatch.com/story/americans-are-still-terrible-at-investing-annual-study-once-again-shows-2017-10-19 Licensed Insurance Professional. This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation. By providing your information, you give consent to be contacted about the possible sale of an insurance or annuity product. This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. This information has been provided by a Licensed Insurance Professional and is not sponsored or endorsed by the Social Security Administration or any government agency.  The coronavirus is here. It’s impacted every corner of American life and is likely to continue to do so. Colleges have closed. States are closing schools and banning large gatherings. Businesses are closing or cutting hours. Consider some of the stunning developments from the past weeks:

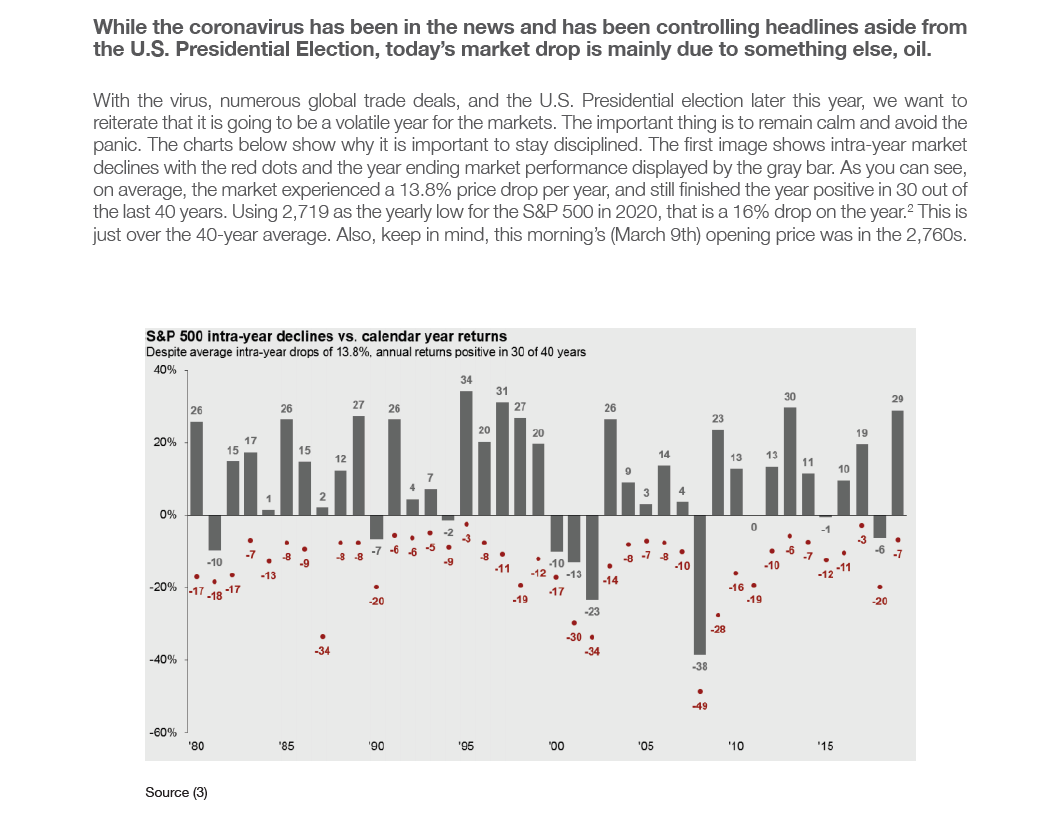

Worldwide, as of Friday, March 13, there are more than 139,000 confirmed cases of COVID-19, which stands for coronavirus disease 2019. More than 1,800 of those cases are in the United States, with 135 new cases in the prior 24 hours.5 The pandemic has had a significant impact on the economy and the stock market. On Friday, February 21, the Dow Jones Industrial Average (DJIA) closed at 28,992. On Thursday, March 12, the DJIA closed at 21,200. That’s a decline of 7,792 points, or 26.87%, officially putting the stock market in bear market territory. What can you do to protect your nest egg from the coronavirus? There’s no way to predict the movement of the stock market, especially in the short-term. However, there are a few things you can do to minimize your exposure to risk. Don’t panic. It may be tempting to sell all your investments and look for safety. However, take some time to explore your options before you make an impulsive decision. Bear markets happen, but they’re temporary. The average bear market lasts 13 months and is followed by a 22-month recovery.7 However, not all bear markets last that long. The 1987 bear market that contained the famous “Black Monday” crash lasted only 3.3 months and was followed by a 30-month bull market. The 1990 bear market that was triggered by the Gulf War lasted 2.9 months and was followed by a 113-month bull market that saw the S&P 500 rise by 417%.8 Of course, there are longer bear markets as well. The 2007-2008 bear market that was triggered by the financial crisis lasted 17 months. It was followed by the bull market that just ended, which lasted nearly 11 years and saw a 400% increase in the S&P 500.8 It’s impossible to know how long this bear market will last or how far the markets will fall. However, if history is any guide, the bear market will end at some point and the markets will recover. If you pull completely out of your investments, you may miss the recovery and the beginning of the next bull market. Review your allocation. When’s the last time you adjusted your allocation? Many people become more risk averse as they become older, even without the threat of the coronavirus. You don’t have to sell all your investments to reduce your risk. You may be able to achieve that goal by making slight changes to your allocation. If you haven’t adjusted your allocation in years, now may be the time to do so. You may want to slightly adjust to assets that are historically less volatile. A financial professional can help you find the right allocation for your risk tolerance. Consider risk protection tools. There are some financial vehicles out there that are immune to the coronavirus, and all other forms of market risk for that matter. For example, there some types of fixed annuities that allow you to earn interest based on a stock market index’s performance. If the index performs well, you may earn more interest. If it performs poorly, you don’t lose money. Again, a financial professional can help you determine if these tools are right for you. Ready to protect your nest egg from the coronavirus? Let’s talk about it. Contact us today at Walker · Wells. We can help you analyze your investments and implement a strategy. Let’s connect soon and start the conversation. 1https://www.google.com/search?safe=off&tbm=fin&sxsrf=ALeKk000JGptVKZkoj4o7x5-9JnJ9uG0oQ:1582753229486&q=INDEXDJX:+.DJI&stick=H4sIAAAAAAAAAONgecRozC3w8sc9YSmtSWtOXmNU4eIKzsgvd80rySypFBLjYoOyeKS4uDj0c_UNkgsry3kWsfJ5-rm4Rrh4RVgp6Ll4eQIAqJT5uUkAAAA&sa=X&ved=2ahUKEwjzzIagl_DnAhVHaM0KHR-vA0YQlq4CMAB6BAgAEAE&biw=1366&bih=641&dpr=1#scso=_6OVWXrG8OdeqtQad9q_wAg1:0 2https://www.msn.com/en-us/money/markets/trump-reportedly-furious-about-stock-market-plunging-on-coronavirus-fears/ar-BB10o1pg 3https://www.marketwatch.com/story/why-a-supply-shock-is-biggest-stock-market-worry-as-viral-outbreak-continues-2020-02-25 Annuities contain limitations including withdrawal charges, fees and a market value adjustment which may affect contract values. Annuities are products of the insurance industry; guarantees are backed by the claims-paying ability of the issuing company. Guaranteed lifetime income available through annuitization or the purchase of an optional lifetime income rider, a benefit for which an annual premium is changed. Licensed Insurance Professional. This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation. By providing your information, you give consent to be contacted about the possible sale of an insurance or annuity product. This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. This information has been provided by a Licensed Insurance Professional and is not sponsored or endorsed by the Social Security Administration or any government agency. 19868 - 2020/3/2 |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

June 2021

Categories |

RSS Feed

RSS Feed

Melinda J. Wells

Financial Advisor

Walker Wells Insurance, Investment & Financial Advisory Firm

Financial Advisor

Walker Wells Insurance, Investment & Financial Advisory Firm

3918 N 750 E,

Buhl ID 83316

Buhl ID 83316

208-328-6913

mwells@aisgadvisor.com

mwells@aisgadvisor.com

|

Securities & Advisory Services Offered Through: American Independent Securities Group, LLC (AISG) Member FINRA/ SIPC. AISG is a SEC registered investment advisor. P.O. Box 579 Eagle, ID 83616. Walker Wells is not Affiliated with AISG.

Please note that not all the services and products mentioned in this site are available in every state. Representatives may transact business, which includes offering products and services and/or responding to inquiries, only in state(s) in which they are properly registered and/or licensed. The information within this website has been prepared for informational purposes only and is not an offer to buy or sell, or a solicitation of an offer to buy or sell any security or instrument or to participate in any particular investment or trading strategy. Licensed in AK; AZ; ID; MN; MT; ND; OR; SC; WA |

|